A COMPLETE INCOME STATEMENT: DISCLOSURE AND PRESENTATION

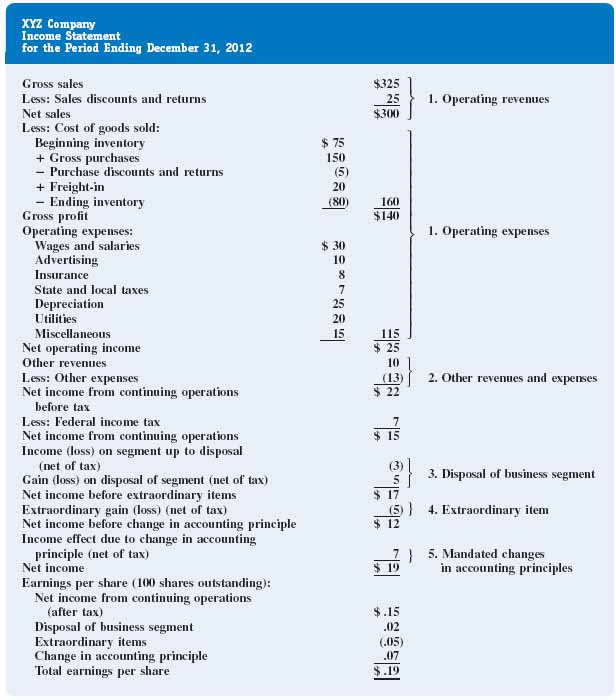

Figure 13-4 provides an income statement that contains each of the five categories introduced in the previous section. Review the statement carefully. The following discussion first considers the income statement in general and then covers each category individually.

5. A recent financial standard requires that the financial effects of discretionary accounting changes should no longer affect net income.

FIGURE 13-4 A complete income statementa

aMost real-world income statements are variations of two basic formats: (1) single-step or (2) multistep. This income statement uses the multistep format. Under the single-step format, all revenues and expenses above “net income from continuing operations” are grouped into two separate categories. Below “net income from continuing operations,” the two formats are identical.

The computation of net income on the income statement involves five major components, each representing one of the five categories. In general, as one moves from the top to the bottom of the income statement, the events become increasingly less important to the operations of the business. Net operating income (operating revenues less operating expenses) reflects financial performance resulting from transactions that are both fundamental to a company's normal activities and occur frequently. Other revenues and expenses ...

Get Financial Accounting: In an Economic Context now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.